Precious metals are apparently waking up. And here is where you can find the best deals.

Site:

Precious metals news

U.S. banks are sitting on a powder keg larger than the one that exploded in 2008, how you can prepare for the coming collapse.

Sub-normal and now negative interest rates distort asset prices. Investors are crowded out of low-risk assets and crowded in to higher risk assets

Monetary policy is suffering from diminishing returns. It's time for governments to act.

Several economists for the International Monetary Fund (IMF) recently expressed concerns about moving interest rates into negative territory. They believe it could backfire on the European Central Bank (ECB), making banks less profitable overall and reducing lending.

So the next round of experiments will probably feature bigger deficits and more aggressive public hand-outs. Which – since these have already been tried and failed – doesn’t give much hope for the future.

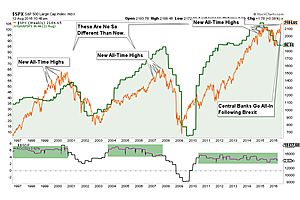

It’s pretty amazing when you think about it for a moment. All three indices hit simultaneous new highs at a time when earnings, profitability, and economic data are deteriorating.

In the middle of a prolonged period of negative real interest rates & loose monetary policy, fears are rising that asset bubbles are being created.

The glue binding a still-aggressive global monetary policy response to a struggling world economy & almost daily record highs for world stock markets along with record low bond yields is set to remain intact in the coming week.

Aug 15, 2016 - 12:05:10 PDT

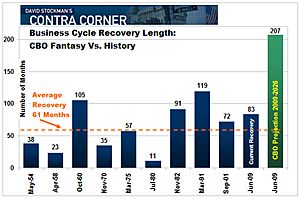

Here follows a deconstruction of Rosy Scenario. It underscores why the nation’s entitlement based consumption spending will hit the shoals in the decade ahead.

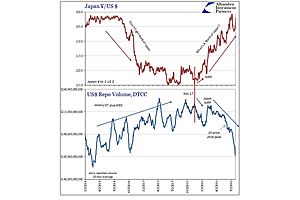

Repo fails are an indication of collateral “tightness.” Dealer net long inventory is an indication of collateral hoarding.

With negative interest rates, governments, and some high quality corporates, are now being paid to borrow money.

In this interview with Kennedy Financial, Eric Dubin warns, "We're in the End Game Right Now"...

Jim Rickards takes you behind the scenes at the IMF and why “they have no interest in commenting publicly about what is really going on.” Read on.

“We’ve been bulls on 30-year Treasury bonds since 1981 when we stated, “We’re entering the bond rally of a lifetime.” “Their yields back then were 15.2%, but our forecast called for huge declines in inflation and, with it, a gigantic fall in bond yields to our then-target of 3%.” “It’s still under way, in our opinion.” – A. Gary Shilling Let’s take a look today at just how attractive U.S. interest rates are relative to most of the world. To wit, the title of today’s piece, “The Best Looking Dude at the Dance.” Who in their right mind could have imagined that 1.50% would be attractive? We’ll look at the comparisons today and consider the implications. Lower for longer? Dr. A. Gary Shilling says yes. I’m getting concerned that too many are now in that camp (yours truly among them). The bond market seems to have forgotten last Friday’s strong employment report. The worry about “What Would Janet Do” (raise interest rates) has subsided. The yield on the 10-year

Our Federal Reserve is composed of labor market economists who place their faith in the theory that inflation is spawned from too many people working.

Aug 15, 2016 - 11:06:37 PDT

the status quo could continue for several years yet – if nothing “breaks” in the system" but "without an external economic shock it is hard to see policymakers being prepared to take dramatic, fiscal action to jumpstart the global economy and bounce it out of a financial repression defined by low and falling real yields to one that at least initially is defined by rising nominal yields through higher inflation expectations.

Federal Reserve Bank of San Francisco President John Williams called for monetary & fiscal policy makers to rethink the way they operate, saying America is getting a taste of a new economic normal that warrants a change in orthodoxy.

central bank stimulus, which has distorted bond markets around the world already, may be starting to affect stock markets as well.

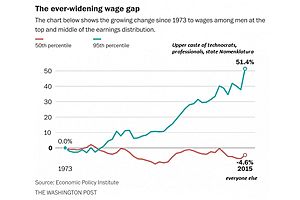

The only way to reverse declines in labor participation and stagnation in wages and demand is to make it easier to start enterprises and hire people.

Yield is going to become ever more scarce, especially if the Fed fails in its mission to raise rates.